He whakamārama mō te kāwanatanga ā-rohe

-

Local government explained

Local government is a crucial part of our democracy, where you can have your say on how your community is enhanced and who gets to make decisions on your behalf.

It’s the way communities make democratic decisions about how their towns, cities and regions work and how they’ll grow and develop.

City, district, and regional councils are governed by representatives elected by you and your community. They’re responsible for making decisions about local or regional activity to ensure a healthy environment, thriving families and businesses, safe spaces for all and a culture that supports every individual’s sense of belonging.

Local government is all about community. It’s about ensuring that the needs and wants of you, your family/whānau and the people in your region/rohe are heard and considered when decisions are made — whether that’s in community discussions, the council chamber or the highest levels of central government.

Why do we need local government?

While there are many things that unite Aotearoa, local government acknowledges and supports the fact that every town, city, district and region is different with unique needs and wants that must be understood by those making the decisions.

It also guarantees that the people making those decisions are elected by the community itself. Ultimately, local government is designed to make sure you’re heard and represented in the decision-making space and have the ability to influence the future of your community.

It’s all about keeping it local.

- Local democracy: local people electing local people to make decisions on local issues.

- Diversity: recognising the diversity that exists across our nation and the diverse circumstances faced by councils including geographical, financial and social.

- Local choice: reflecting the unique needs of individual councils/kaunihera, and to need for public participation in community decision-making.

- Local accountability: local authorities are primarily accountable to the people who elect them - their communities.

What does local government do?

For a lot of people, thinking about councils/kaunihera, immediately conjures images of roads, rubbish and paying rates. This makes sense because these are really important to our day-to-day lives. However, local government is so much more.

In fact, in 2021, councils/kaunihera across the country were responsible for $123 billion worth of assets and employed approximately 30,000 staff. They had a collective spending power of $11.7 billion.

Council’s role is to enable democratic decision-making by and for communities and to promote their social, economic, environmental and cultural wellbeing. In practice, this means everything from footpaths and lighting and the supply of freshwater/wai to resource management and environmental health and safety.

They look after a multitude of community facilities, services, and public spaces we can enjoy — from parks and playgrounds, community centres, libraries, sports arenas and concert halls to beaches and rivers.

Councils/kaunihera also work closely with central government and other organisations, public bodies, businesses and citizens and are the first port of call when things go wrong through local civil defence and emergency management.

How is local government funded?

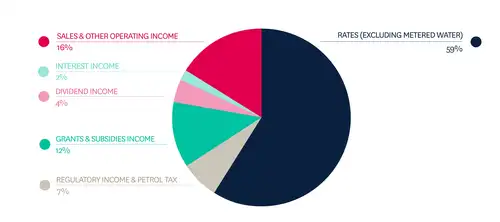

While central government is mostly funded by income and consumption taxes, local government is mostly funded by property. They also receive grants and subsidies, primarily their share of roading taxes and charges, and development contributions.

Councils/kaunihera generate income from things like regulatory fees such as parking fines, the sale of goods and services like swimming pool charges, and interest earned from investments.

Local authority operational revenue by source, year ended June 2018

However, without borrowing and debt many communities would simply not have the infrastructure that enables them to exist and grow.

This is why most councils/kaunihera also borrow from the Local Government Funding Agency, which raises bonds (a loan from an investor to a borrower) and can lend to councils/kaunihera at lower interest rates than those charged by the banking sector.

In 2019, the New Zealand Productivity Commission completed an inquiry into local government funding and financing, including the options and approaches for improving the system. You can read all about the inquiry and its findings here.

If councils borrow today, who is responsible for paying it all back?

All councils/kaunihera grapple with the decision over what proportion of capital expenditure should be paid by operational income and what should be paid for by debt, whether by bank loan or bond.

In deciding, they apply the principle of inter-generational equity: that is, each generation that benefits from an investment, should contribute to the cost of it.

For example, the cost of investment in a wastewater plant that is expected to serve a community for at least 50 years, should be covered by generations spanning those 50 years.

One way of doing this is to borrow and pay it off during the 50-year lifetime of the plant, ensuring that each generation which benefits also contributes.

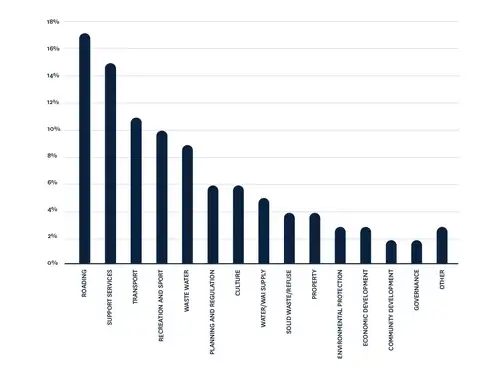

What does local government spend its budget on?

Expenditure differs from one council/kaunihera to another depending on size and demographic makeup.

Stats NZ have developed an interactive tool that shows how councils spend their rates income. You can explore individual council spending here.

In 2018, the costs of council/kaunihera activities across the country were as summarised below.

Local authority operational revenue by activity, year ended June 2018

How does local government differ from central government?

Firstly, some similarities. Both are established by Parliament with their roles and powers defined in legislation. Both are made up of people voted in by you.

However, while those in central government are responsible for national priorities and decisions, people in local government are responsible for community priorities and decisions, and they are accountable to their communities.

In many instances, central government sets a national policy or standards that are then applied by local government in a way that suits the needs of their community.

Take the transport system for example. Central government sets the direction in the Government Policy Statement on Land Transport. Central agency, Waka Kotahi, then prepares the National Land Transport Programme. From here, Regional Transport Committees translate national goals into meaningful regional plans which are supported by councils/kaunihera. Another comparison is around how local and central government manage significant assets and undertake commercial activities. While central government does this through State-owned enterprises like Transpower, Kiwirail, NZ Post and Metservice, Councils can establish local and regional publicly owned corporations known as Council-controlled organisations, or CCOs.

Then there is funding – while central government is funded by a number of taxes, local government is mostly funded by rates – money collected from property owners.